MOST RECENT BLOGS

Check out our video resources to learn more about the buying and selling process

Fundamental Questions To Ask Before Hiring Professional Movers: Part 2

Do you use subcontractors or a third-party to handle and deliver my belongings? Before you work with a mover, you need to know how they operate and if a different company will actually be doing the loading, transporting, and unloading of your belongings. This is because while many moving companies h

Read MoreFundamental Questions To Ask Before Hiring Professional Movers: Part 1

Once you've bought a home, there’s nothing that could be more stressful than moving. This is why it's a no-brainer to hire a professional moving company to help you with your valuable possessions, especially if you’re making a long-distance or interstate move and you’ve got bulky items to bring with

Read MoreHomeowners, Make Sure You Leave These Repair Tasks To The Pros

There are several reasons why homeowners choose to DIY various home repair projects. It might be due to budget limitations, to save money, or just to enjoy a good challenge and proudly build sweat equity. However, substantial tasks are considered too technical, too difficult, or just too unsafe to b

Read More5 Best-Kept Strategies To Make The Most Money When Selling Your Home

Savvy home buyers and sellers often have the same goal: to get the best price possible for and out of their biggest investment. For many sellers specifically, it means selling their home for top dollar and within their predetermined time frame. To achieve this, it's necessary to implement the right

Read MoreIs Downsizing Right For You? 5 Questions To Ask Yourself Before Making The Move

There's a host of reasons many homeowners choose to downsize. Perhaps they’re going to retire soon or their kids have already flown the coop. There’s no need for the extra rooms anymore; cleaning and maintaining them can also be costly. Or maybe they’ve looked at their recent electricity bills and t

Read More5 Simple but Essential Minimalist Design Tips To Embrace In Your Home

It's halfway through the year, and you’re probably one of those homeowners who’d already forgotten about their New Year’s resolutions to keep their home more organized. Or you’re a new homeowner who has just packed and moved to a new place and realized you have way too much stuff even if you don’t w

Read More5 Rookie Mistakes To Avoid When DIY Painting Your House

Adding a fresh coat of paint is one of the cheapest and easiest ways to give your home the makeover it deserves. It breathes new life into your space, no matter if you're painting the interior or exterior of your home. Whether you are a typical homeowner who wants to refresh your space or a seller w

Read More-

In the midst of a global pandemic, our homes have become much more than a space that provides a roof over our heads. We've experienced sheltering in place for several months, so having a place we can call our own has become invaluable. For many, our homes have also turned into our workspaces and eve

Read More The Complete Final Walkthrough Checklist

You're almost there. You can’t wait to finally get your house keys and move to this new place you’d call home. You just can’t contain your excitement as the closing day approaches. However, you’ve still got the final walkthrough—your last chance to make sure everything is in place and in the right

Read More6 Mistakes to Avoid When Buying Furniture for Your New Home

Selecting and buying furniture for your beautiful abode, whether it be a sofa, dining table or any other piece, is no doubt fun and exciting. Especially if you're a first-time homeowner who finally has the liberty to choose whatever furniture you want to fill your private space with. But before you

Read MoreShould You Renovate or Not? Here Are 3 Things To Consider Before Selling Your House

When thinking about putting their property on the market, homeowners often need to ponder on this question: should they renovate or not before selling? Since it's every home seller’s goal to make sure they get the best price for their biggest investment, it’s important to determine whether you shoul

Read MoreThe Risks of Buying A Home With Unpermitted Renovation Work

When you're on a search for your dream home, it’s easy enough to fall in love with any renovated features, such as a remodeled kitchen or bathroom, a finished basement, or a newly-installed deck, that are set to make your life more comfortable once you take over as the owner. However, those lovable

Read MoreCurb Appeal Tips To Show Your Home In Its Best Light When Selling

When it comes to selling a home, first impressions make a huge difference. And sometimes, you only have one shot to convince a potential buyer to take a look at your home and step inside it. You want your property to have a “wow” factor to entice them to inquire further. This is where your curb appe

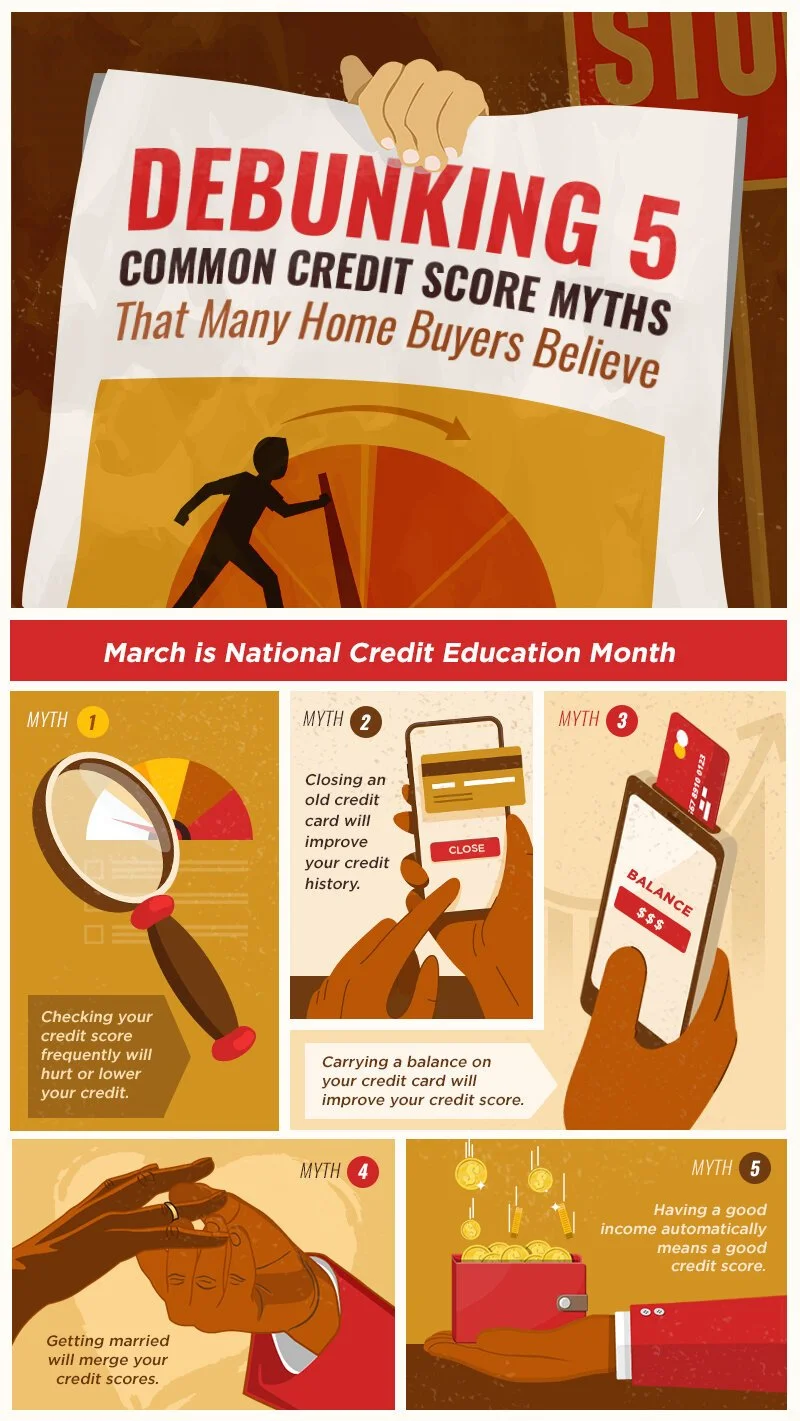

Read MoreDebunking 5 Common Credit Score Myths That Many Home Buyers Believe

When it comes time to buy a home, a good credit score boosts your chances of getting a mortgage because it shows lenders or mortgage companies that you are likely to pay a loan on time. Thus, having a bad credit score can be a massive barrier towards homeownership. This is why understanding and mana

Read More5 Cleaning Habits You Need To Break for Better Housekeeping

Cleaning is tough, but it's something we need to do consistently to take care of our humble abode. Not to mention it’s a crucial task to keep our family and home safe in this pandemic age. But since it’s a tedious job, we’re often guilty of cutting corners to do it “faster” and easier. This could r

Read MoreHow To Get Over The Heartbreak of Losing Out on Your Dream Home

It's already stolen a piece of your heart. You’ve spent countless hours thinking about it. You know it’s a huge commitment, nothing like you’ve ever had before, but you’re more than ready for it. You had such big dreams and imagined the two of you growing old together. But then you lose out. Maybe

Read MoreTop 5 Situations Where You Should Accept the First Offer on Your Home

It's natural for many sellers to be hesitant to accept the first offer they receive on their home. They may want to entertain multiple offers from interested buyers and could even be thinking about potential bidding wars. In certain circumstances, however, the first offer on your home may actually

Read MoreLetting Go of the Home You Love: Tips To Deal with the Emotional Impact of Selling Your House

Your home may be your biggest financial asset and investment, but once you decide to sell, everyone will agree that it's also more of an emotional journey. After all, you’re not just leaving a home that you loved—you’re ending a “love affair” with a place you’ve had for a long time and have lots of

Read More5 Things That Could Go Wrong If You Skip Hiring A Real Estate Agent To Buy A Home

If you are thinking about buying a house this year or even in the near future, one of the things you might have been asking yourself is whether you need to hire a real estate agent or not. After all, you know how to browse through online listings (which is something you might already love doing duri

Read More6 Doable Resolutions To Help You Save For A Down Payment on A Home

Having enough money to put as a down payment is one of the biggest roadblocks to purchasing a house, especially to first time buyers. If you're one of the many people who aspire to turn their homeownership dream into a reality, you probably know that among the many things you need to start doing is

Read More

Categories

Recent Posts