MOST RECENT BLOGS

Check out our video resources to learn more about the buying and selling process

Home Sellers: Check This Easy Guide To Boost Your Home's Curb Appeal

Like moths attracted to flames, potential buyers can get riveted to a home with an excellent curb appeal. Buyers who will be drawn to your home's appearance will definitely want to discover more of what lies behind your front door. Fortunately, maximizing your home’s curb appeal doesn’t necessarily

Read MoreTop 7 Reasons Why You Shouldn't Overprice Your Home

Tempting as it may seem, jacking up the listing price of your home to leave room for negotiations is a dangerous risk that a lot of sellers regret taking.If you are really serious about selling your home, it is best to take pricing seriously by listing your home at its fair market value. Otherwise,

Read MoreUnderstanding Contingencies: A Guide For Buyers and Sellers

When looking for homes online, home buyers might chance upon a property with a “contingent offer” status. This means that an offer has been made and accepted, but the sale is still conditional while both parties work on meeting certain criteria. These criteria, or contingencies, are actions that mus

Read MoreGetting Cold Feet? Here's How You Can Prevent Seller's Remorse

Buyer's remorse (the feeling of regret after making a huge purchase) is a common sentiment that a lot of people understand and sympathize with, given that the average person makes huge purchases more often than he/she gets to sell anything of substantial value. This is why the seller counterpart of

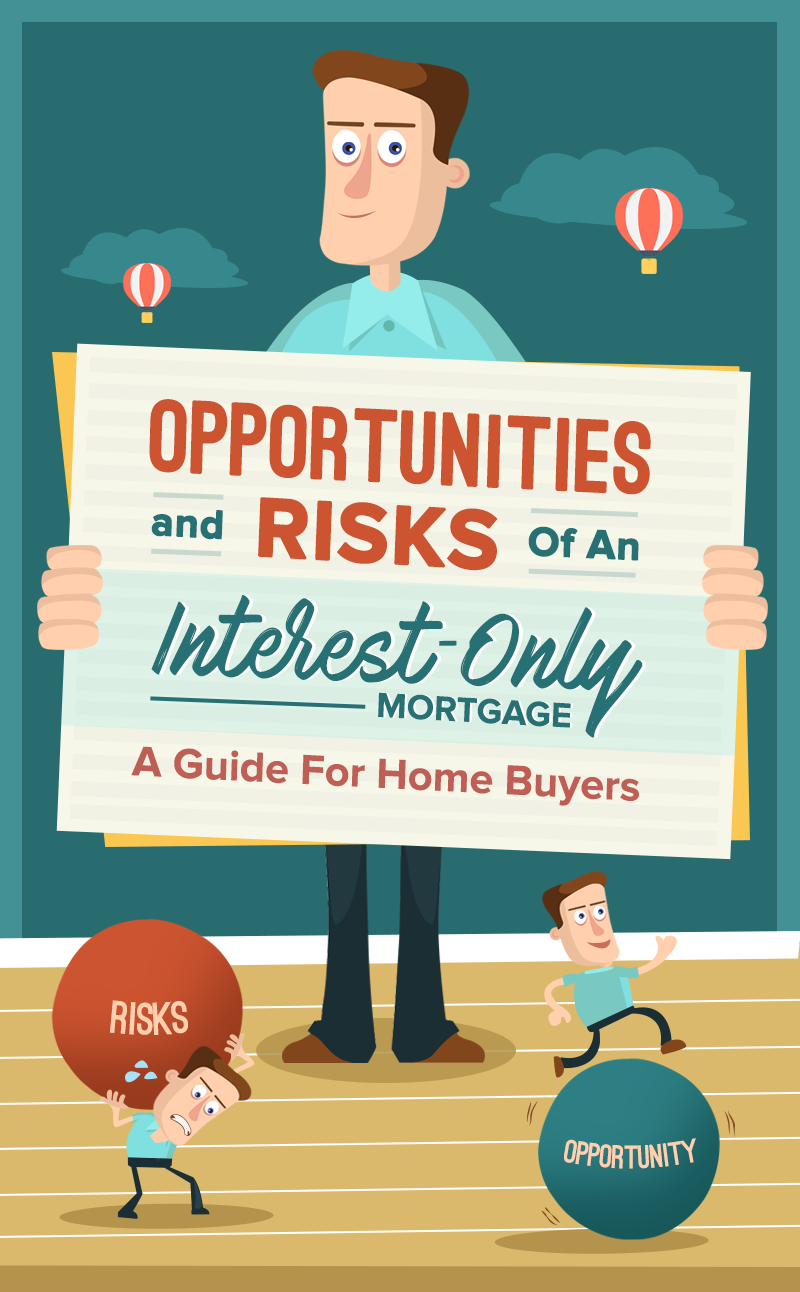

Read MoreOpportunities And Risks Of An Interest-Only Mortgage: A Guide For Home Buyers

Opportunities 1. Lower monthly payments The main and obvious advantage of an interest-only mortgage is its low monthly payments. This benefits buyers who are looking to buy a relatively expensive property, since an interest only loan allows you to buy a pricier house than you would be able to affo

Read MoreIn Love With Historic Homes? Here Are The Pros And Cons Of Buying One

Owning a historic home certainly comes with its own set of benefits and challenges. You need to make sure that you are ready for the challenges and responsibilities—financially, emotionally and even physically. Beyond its unique and charming characteristics, it is also important to determine wheth

Read MoreThe Beginner's Guide To Escrow in Real Estate

What is escrow and how does it work? At some point in a real estate transaction, you will encounter the word “escrow.” If you're the buyer and you make an offer on a home you like, you’ll provide an earnest money deposit in the form of a check that will be placed in this escrow. But what does it rea

Read More12 Telltale Signs It's Already Time For You to Move

According to the U.S. Census Bureau in 2016, more than 42 percent of people said they moved for a housing-related reason. Many of them either wanted a new home or a better apartment. Other reasons people cited for moving include family and employment-related reasons. “The decision to move can be per

Read More7 Secrets To Getting A Mortgage Without A Full-Time Job

Let's face it: there’s already a growing number of freelancers, contract workers, and gig economy workers in the U.S. It’s not surprising, given that many people now want to be their own boss or work from their own homes while sitting comfortably in their sofa. In a 2017 survey conducted by Upwork a

Read MoreHow To Successfully Buy A Home In A Seller's Market

Planning to buy a home while the market is tight? Don't dive in unprepared! Understand what makes up a seller’s market, and follow a plan to make your offer stand out. A lot of home buyers tend to make rookie mistakes that get their offers rejected in a seller's market. If you want to be successful

Read MoreHow To Determine The Best Time To List Your Home For Sale

Much like any business venture, listing your home for sale is all about finding the best possible timing. The best case scenario would be one in which the sale happens while the market is at its best, at the same time you are prepared to leave, and to buyers that are motivated to pay more. However,

Read More10 Smart Tips For Buying A New Construction Home

In an analysis conducted by the National Association of Home Builders (NAHB), it was found that there was a larger percentage of new homes, especially single-family homes, that cater to the preferences of many home buyers today. Significantly, new construction is addressing the substantial demand fo

Read More10 Thoughtful and Heartwarming Gift Ideas for First-time Homeowners

The spring real estate market is already here. Despite the strong competition, it's a great time for home buyers to score their dream home because of high market inventory. And soon, there will be fresh batches of buyers who have just finished closing and will soon be moving. Purchasing a new home i

Read MoreHow To Sell Your Home And Buy One At The Same Time (Or In The Quickest Possible Succession)

For some people with enough funds and other houses to live in, selling a home and buying one at the same time can be relatively easy since there is not much pressure involved. But for those who need the equity from their old house to buy a new one, things can get quite stressful--especially so when

Read More3 Most Important Things To Remember When Selling A Home That You Still Have To Live In

luxury of living elsewhere while selling the house they do have. It's pretty common for home sellers to have to deal with the challenge of selling the same home in which they still have to eat, sleep, and bathe in -- so it’s nothing to be embarrassed about. However, it can be quite a challenging fea

Read MoreWhat's In A Mortgage? Breaking Down the Components of A Mortgage Payment

In simplest terms, a mortgage is a long-term loan designed to help borrowers purchase a house. It allows individuals to become homeowners without making a large down payment and thus, fulfilling The American Dream. Once you become a homeowner, a mortgage represents one of your life's biggest financi

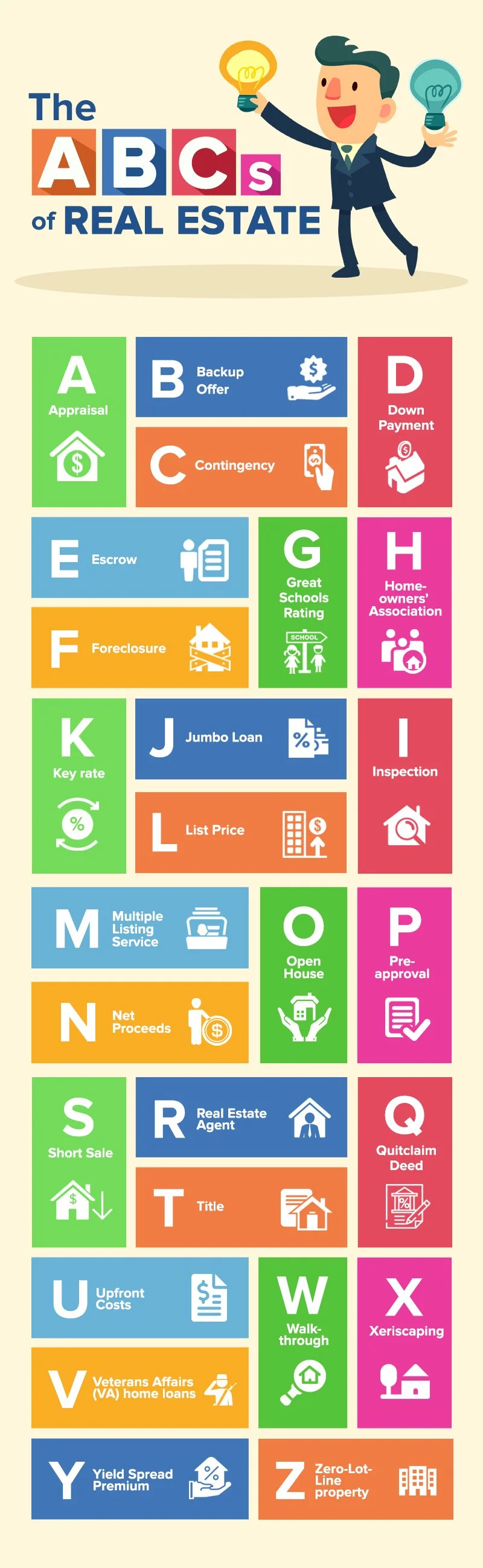

Read MoreThe ABCs of Real Estate: Real Estate Terms Every Buyer And Seller Needs To Know

Whether you are a first-time home buyer or a third-time home seller, the real estate transaction can be confusing and stressful enough even without the many terms and acronyms used during the process. But don't be overwhelmed — we’ve compiled a mini-glossary of the important terms you should know an

Read MoreSelling Your Home? Here's How You Can Upgrade Your Kitchen On A Budget

The kitchen is one of the most important areas in a house. If a potential buyer is someone who spends a lot of time in the kitchen, the condition of this area can make or break a sale. In fact, even if the buyer is not much of a cook, the kitchen is still a major consideration since this is where fr

Read MoreTop 5 Things Home Buyers Forget To Check During Home Viewing

The viewing is usually the most exciting part of looking for and purchasing a home. It is the biggest purchase anyone ever makes, and home sellers usually go above and beyond when staging their homes. Because of this, home buyers find it so easy to fall in love with a home that looks great at first

Read More20 Smart and Simple Ways You Can Start Saving For A Down Payment On A Home

You may think that buying a house still isn't in your realm of possibility. In fact, you may even feel a wave of panic just thinking about where to get the money for your down payment. For many young people, saving up to buy a house is the least of their priorities, especially when you’re still in d

Read More

Categories

Recent Posts